Procedure for WHT return in Poland - does it really have to be so difficult and complicated? Not necessarily. We explain this issue in our next infographic. We hope that it will be helpful for you. If you have any doubts, please contact us. We will be happy to answer your questions.

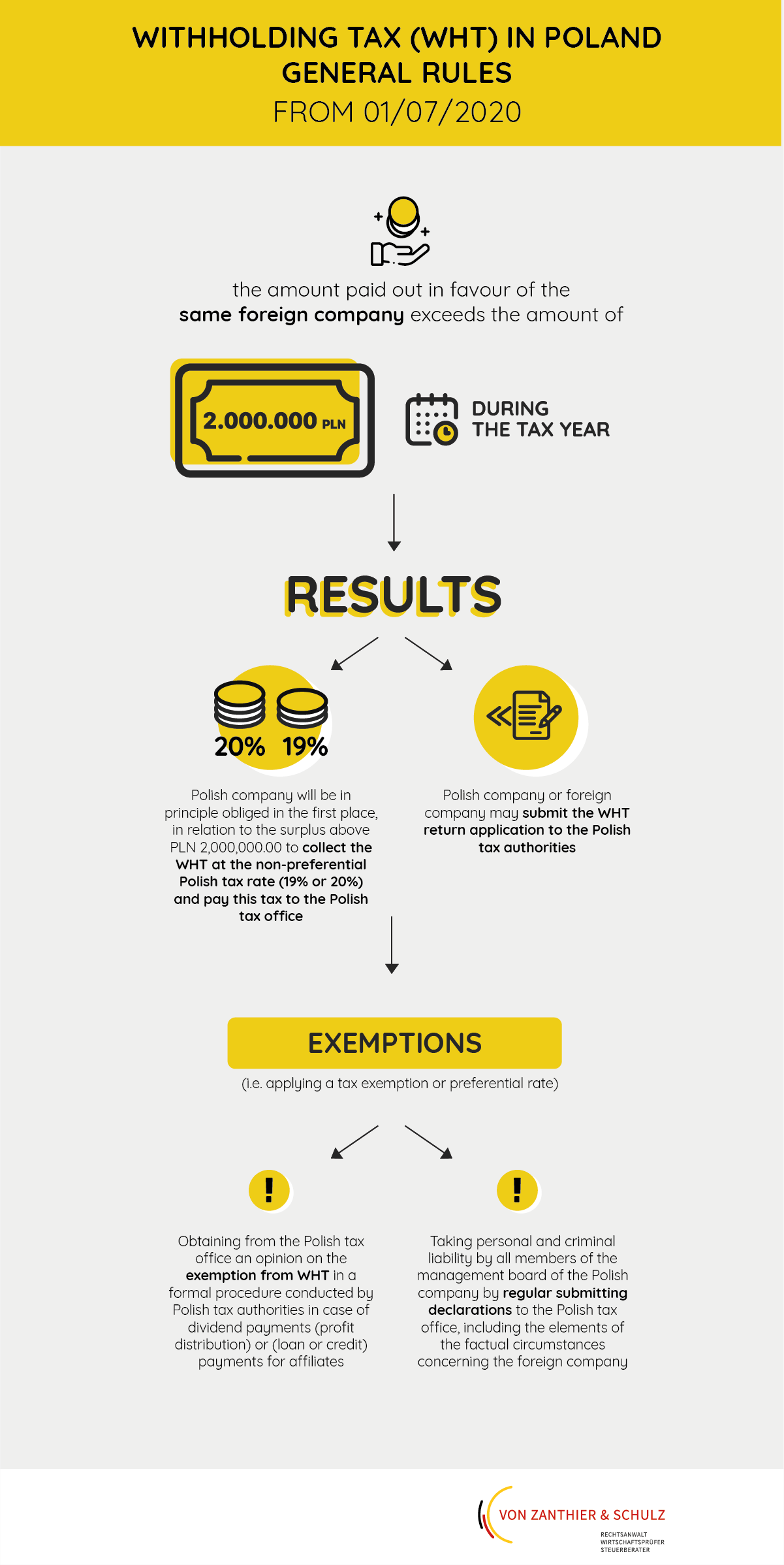

From 01/01/2020 some payments (e.g. interest, dividends, royalties) made by a Polish company to a foreign company in the amount above 2.000.000 PLN during a tax year shall be in principle taxed at the non-preferential Polish tax rate (19% or 20%). When a taxpayer had the right to apply a preferential rate (e.g. 5%) or WHT exemption, it is possible to apply for a WHT refund in the following procedure:

• collecting of some documentation to prepare the application (e.g. certificate of tax residence from the state of the payment’s recipient, documentation regarding bank transfers, written statements regarding the payment’s circumstances);

• preparation of a formal WHT return application by a Polish or foreign company;

• submitting the application in electronic form to the Polish tax authorities;

• if necessary, completing the application with additional information and documents requested by the Polish tax authorities.

Results:

1) obtaining a WHT tax refund decision:

a) decision is issued within 6 months from the date of application’s receipt by the Polish tax authorities;

b) the Polish tax authorities may extend the refund period, including through prior tax control (also on the territory of a foreign company) or by asking foreign tax authorities for additional information;

2) decision about refusal of WHT tax return: in such case there is a right to appeal against the refusal.

{kind=link}

{kind=link}

{kind=link}

{kind=link}